I might as well write about this old, classic sum-of-the-parts investment too. It’s well known in the value investing community, so nothing new here either except a fresh update.

For those who this is new to, it’s a conglomerate that is run by the Tisch family. Of course, I think many people know Larry Tisch, especially those living in New York City. He once owned and ran CBS. Tisch is one of those value investors that really dug into things and took large stakes in what he liked. There is a lot written about him including a pretty good book (here’s a link: Book about Tisch).

Laurence Tisch passed away a few years ago but Loews is now run by three of his sons with James Tisch as CEO. They have stuck to the strategy of investing in value situations and going in big when the opportunity presents itself. One big homerun for them they still own is Diamond Offshore, which started out as an outfit that just bought oil rigs that nobody wanted at very, very low prices in the 1990s. The industry was basically dead with crude oil prices low. By the time crude oil prices soared, they had a bunch of rigs that suddenly became very valuable. This is what they do; find stuff cheap that nobody wants, but that has potential to create great value.

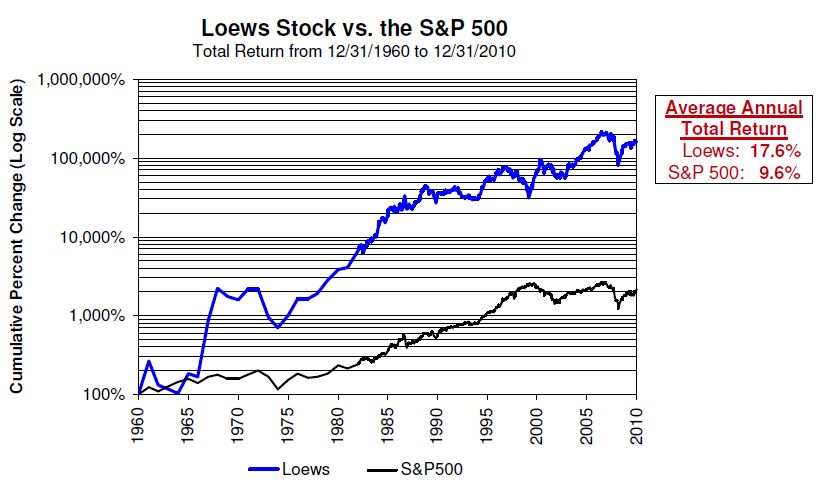

Their 2010 annual report is a great summary of what they are. $1 invested in Loews Corp stock on December 31, 1960 was worth $3,300 by the end of 2010. $1 invested in the S&P 500 index at the same time would have grown to a not-so-bad $97.

Annualized, Loews Corp stock grew +17.6%/year over 50 years versus +9.6%/year for the S&P 500 index, an incredible outperformance over an incredibly long period of time.

The above chart was just cut and pasted from the annual report; it shows the value creation machine that Loews Corp is.

Of course, people will immediately say that a lot of outperformance seemed to have come in the early years; what about more recently?

Here are the returns of Loews Corp common stock versus the S&P 500 index over recent time periods:

Loews Corp S&P 500 (incl dvd)

5 year annualized return +5.0% +2.3%

10 year annualized return +9.4% +1.4%

20 year annualized return +9.9% +9.2%

So Loews Corp outperformed the index by +2.7% in the recent five year period through the end of 2010 and +8.0% for the ten year period. The twenty year period outperformance is only +0.7%, however. I wouldn’t worry about that too much as some time period performance figures may be sensitive to time period beginnings and endings. Loews does seem to outperform pretty consistently over many time periods.

This is not bad at all in what has been a rough five years for Loews as they do own a large stake in CNA, which is an insurance company which had some balance sheet issues during the crisis.

Here are some interesting links:

Loews Corp overview

Presentation

I often get annoyed when I read a blog and am directed to this link and that link and all the links lead to long reports and things like that (unless they are things I am really, really interested). So I try to avoid that, but the above links are really simple. No reading at all; just simple diagrams that show the structure and value of Loews Corp. Doesn’t take more than a few minutes to skim through it.

Anyway, the above return figures are based on stock price, not book value per share or other fundamental metric. Why is that? I only used the stock price because that’s what Loews Corp uses to show long term returns, and book value per share is not readily available over the long term. Also, book value per share may not reflect the value of the businesses as Loew’s main consolidated subsidiaries are listed on a stock exchange. (In Berkshire Hathway’ case, their stock investment portfolio is marked-to-market on the balance sheet every quarter. However, L’s stockholdings are consolidated subsidiaries; this means the stock prices are *not* marked-to-market and instead the balance sheet and income statements are consolidated into L’s financial statements)

In any case, stock price is fine to see long term returns in this case.

But then, of course, when you go and buy the stock, you have to understand what the stock price represents, or what the intrinsic value of the business is.

Before I update the value per share of Loews, let me just add that I have been following the Tisch family for years and they are very, very shareholder friendly. In fact, since 1971, the number of shares outstanding has gone from 1.3 billion to 413 million shares. As you know, share repurchases at good prices is capital ‘returned’ to shareholders. If a shareholder does nothing, their stake in the business goes UP due to share repurchases.

And the Tisch family is very price sensitive. They are very, very anti-fad and anti-trend. You will never hear any of them spit out platitudes and the latest business fashionable lingo. They don’t do things because everyone else is doing it. They don’t do things to protect their jobs. They are very single-minded in value creation and are very disciplined about it.

One thing, though, that I always scratch my head is that their CNA subsidiary, the insurance company, seems to always be going in and out of trouble. One restructuring after another seems to happen. They have owned this business since the 1970s, so I wonder what’s going on there.

But all this value has been created over the years despite that.

Anyway, let’s take a quick look at what Loews is worth.

Their listed subsidiaries are CNA, Diamond Offshore (DO) and Boardwalk Pipeline Partners (BWP) and this is what they own:

number of shares price value

CNA 242.5 million $22.56 $5.469 million

DO 70.1 million $54.02 $3,787 million

BWP 102.7 million $24.81 $2,548 million

Loews currently has 404.9 million shares outstanding, so including BWP class B shares (not in the above list), the value per share comes to $30.55/share.

The current price of Loews is $34.43/share, so the value of the listed subsidiaries account for most of the value of the stock of Loews.

What else of value is there at Loews? From the June 2011 presentation, which breaks out the value per share of assets that aren’t listed subsidiaries, there is the following:

Value per share

Net cash & investments $9.08

Highmount $3.52

Highmount is a natural gas exploration and production company. Net cash & investments include cash that can be used for future acquisitions, and they do have an investment porfolio of common stocks that is managed from a value standpoint.

Anyway, put these together and you have a value of $30.55 + $9.08 + $3.52 = $43.15 / share in value. It is important to note that the above values exclude things like Loews Hotels, General Partnership interest in BWP and $100 million of subordinated debt of BWP.

So for a price of $34.43, you get asset value of $43.15/share, a 20% discount.

Old time value investors will warn you, though, that L *always* trades at a discount to the sum-of-the-parts.

Taxes?

Some people use 20-30% discount for taxes on the listed subsidiary holdings. I do that too, as you may have noticed for usual sum-of-the-parts analysis. However, Loews management never accounts for taxes and the reason is simple. I don’t think the Tisch’s would do a deal where they have to pay taxes! They would structure any deal to be a tax-free spinoff or similar structure.

What do you own here?

So by owning L, what do you really own? You own a collection of businesses at a 20% discount that may never close. So what’s the point?

First of all, let’s take a quick look at the assets. The largest piece at 40% of the market cap of L itself is CNA, an insurance company. This trades, currently at 0.5x book value, which is pretty cheap. Sure, all insurance companies are cheap and CNA has a history of problems.

But with the Tisch family owning 90% of it, you can be sure they do work very hard to fix it up. They have said that they fixed the problems and CNA should do well going forward. If the insurance market starts to pick up, there can be some nice upside in CNA shares.

I haven’t analyzed CNA closely myself, but during a conference call recently, James Tisch, the current CEO of L was asked where the upside in L may come from going forward. Tisch said that CNA has a lot of potential as the stock price is trading very cheap and since they fixed a lot of the problems, an improvement in the industry fundamentals may provide a boost to returns there.

How about Diamond Offshore (DO) and Boardwalk Pipelines? Diamond Offshore had a tough time recently after the BP explosion in the gulf and all drilling seemed to stop there. DO had to move rigs to international markets outside the gulf. Also, the recent weakening in the global economies is putting some downside pressure on crude prices.

But as I showed in my crude oil post recently, the further out contract months for crude oil still show a tight market going forward; crude will get more expensive to find and drill. Any cyclical slowdown due to economic weakness will probably prove temporary as global trends for higher per capita income and per capita usage of energy will continue to trend up over time.

L’s natural gas businesses too, will likely benefit going forward as natural gas seems to make a lot of sense given environmental issues, high cost of crude oil and now doubts about the future of nuclear energy.

In that sense, L’s positions in their natural gas businesses put L in a good place, it seems.

The Future of Loews

In any case, I don’t know that you want to analyze all of L’s holdings in detail to make a decision on whether you want to own it.

I think the key here is in the managment of L; you have to trust that they will do the right thing for shareholders and that they will be very disciplined in their capital management.

By owning L stock, you don’t just own the individual businesses. You are benefiting from the decision-making by some of the best and honest minds in the business. If they see problems in their businesses, they will be proactive in fixing it. If they see an opportunity to sell or spin something off, they will do so. If they see an interesting investment opportunity, they will take it.

This is what you get when you own L and you can do much worse!

(but, as usual, don’t buy a stock you read about on some blog on the internet! Do your own work.)

This comment has been removed by the author.

Hi,

If you leave a contact here I will email you. And I will delete your contact info so bots and others won't use it.