Oops, I did it again. When I made the Missing Manual cover for Berkshire Hathaway, I told myself that it would be the last time I would do that. Things like that can be fun the first time but can get pretty old pretty fast.

But, sorry, I couldn’t resist this time.

When the news hit that 38% of shareholders voted against Dimon’s compensation plan, I was stunned. I was like, “What the…”.

I didn’t actually read the proxy firm reports so I don’t know what it’s all about, but I was surprised. Then Dimon gets quoted calling investors “lazy” for voting according to proxy advisory firm recommendations. After that, the press jumps in and calls Dimon “arrogant”, even after all the trouble his bank caused.

That was enough, I had to make a post. And this is not a Rahodeb sequel (John Mackey, CEO of Whole Foods posting anonymously on a message board); This is not Jamie Dimon posting anonymously (grammer, for one, would be much better).

Dimon is Underpaid

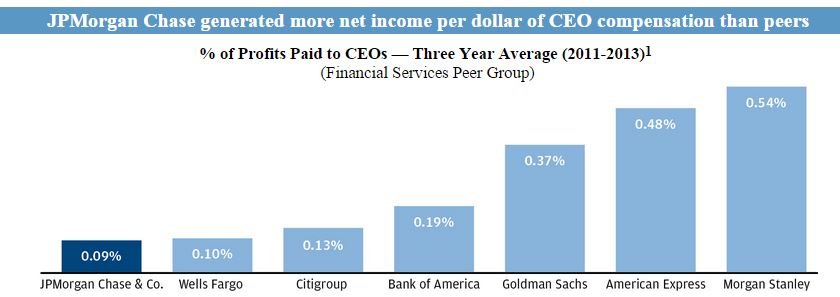

Just in case some were too lazy to read the proxy, here are some interesting charts from it. I found it to be a pretty good proxy compared to many others with minimal explanation of CEO compensation.

Readers here know this because I post this chart all the time, but JPM has been an amazing performer since Dimon came on board. The stock price has also performed very well since the 2007 peak.

…and for this great performance, Dimon gets paid less than any of the other large financial company CEO’s.

…and over time CEO compensation has reflected performance. I didn’t necessarily agree with the pay cut in 2012 due to the whale trade. JPM still made a lot of money that year. I believe in paying for performance, and if the total performance was good, so should the pay. If you run a fund and perform very, very well, you don’t get a pay cut just because you made a mistake and one of your holdings went to zero. That loss is already in the performance number. I think the 2012 pay cut was driven (unfairly) by optics; the board had to do something to show that they were punishing Dimon for making such a stupid mistake. To me, that was totally unnecessary. But I admit there might have been some political value in doing that to appease someone.

Many CEO’s make much larger mistakes and get paid more.

Proxy Advisory Nonsense

I don’t read reports written by proxy advisory firms, so I can only guess, but it seems like they try to create some ideal model and cram everything into the model without much thought. One of them a few years ago criticized the Berkshire Hathaway board saying that they lacked independence. It’s true that all the board members of Berkshire Hathaway are good friends of Buffett. But if the Berkshire board is not acceptable to someone, then they just don’t understand Berkshire Hathaway.

In general, I suppose the proxy advisories are right; the board has to be independent. But for the companies I usually follow, if the CEO needs to be supervised by an independent board, then I don’t want to be invested in that company. This is not the best way to look at things from an academic, corporate governance point of view. But that’s the way I see it, particularly in the cases where I am invested because I like the CEO (in that case, I want him to have more power!).

But anyway, going back to proxy advisory firms, I really don’t understand the business. If you are a professional investor, why would you depend on some outside advisory firm to tell you how to vote? Do they not read the annual reports and proxy statements? Are they too difficult to understand that you need advice from the outside? I don’t get it. Maybe they own too many stocks (hundreds) that they can’t keep track of each one so they need advice. Maybe they are index funds. There must be some history here that makes sense but frankly, I have never really given it much thought.

And then there is this backlash that after causing all this trouble, paying out $20 billion in fines and being charged with a felony (as a firm), bankers are still as arrogant as ever. Well, first of all, if anyone has followed the crisis closely, JPM was one of the good actors. Sure, they may have made some bad loans, even bad subprime loans.

But JPM stayed out of a lot of the problem areas (SIVs) and remained profitable throughout the crisis, not losing money in any single quarter. When the financial industry was on the ropes, JPM stepped in to buy Bear Stearns and Wamu.

JPM got screwed on those deals, because most of the fines that JPM has paid since then have been for things that those two firms did in the past (which was not supposed to happen).

Most people (I notice this from personal conversations with a lot of people too) still look at the banking industry as one large entity, each bank as evil as the other. To most people, there are no good banks and bad banks. All banks are bad. In fact, around here, most people think all big businesses are evil, bank or not. (This is the sort of simplification/generalization that I think is really harmful, like all Muslims are evil etc.).

Individual Prosecutions

And by the way, about these Wall Street violations; a retiring prosecutor said on CNBC the other day that one thing he said he would do differently is to go after individuals instead of firms. When the government goes after companies, the shareholders pay a big fine and the violators get off scot free (actually, those most directly involved are probably fired. But yes, they are free).

Frankly, I don’t understand forcing banks to plead guilty to felonies in the recent foreign exchange case. I think the dealers that were involved should be charged and put in jail, just like for violators of insider trading. No big bank has ever been charged with insider trading (well, at least I don’t remember any cases), but there have been employees caught insider trading and put in jail. Those cases were clear cut, perhaps because they were done for individual gain and not for the gain of the company so it was obvious that the banks had nothing to do with it.

I think if employees were put in jail for violations, this would work better for reducing problems. Nobody wants to go to jail. I am still shocked at the amount of insider trading that was done in the hedge fund world recently, though. I joined the business after the 1980’s scandals, so my generation was terrified of getting caught insider trading.

If a Walmart employee beat up an annoying customer, that employee would probably go to jail. Walmart would not be charged, unless it was proven that Walmart management encouraged such behavior, or maybe that management was negligent in hiring a dangerous person or something like that. Why should a whole company or CEO be charged for things that some employees do? If you own a cab company, no matter how good you are, some of your drivers are going to speed. Some of them are going to park illegally. Some will talk on the cell phone while driving and crash.

Anyway, this is an interesting topic but beyond this single post.

Digression

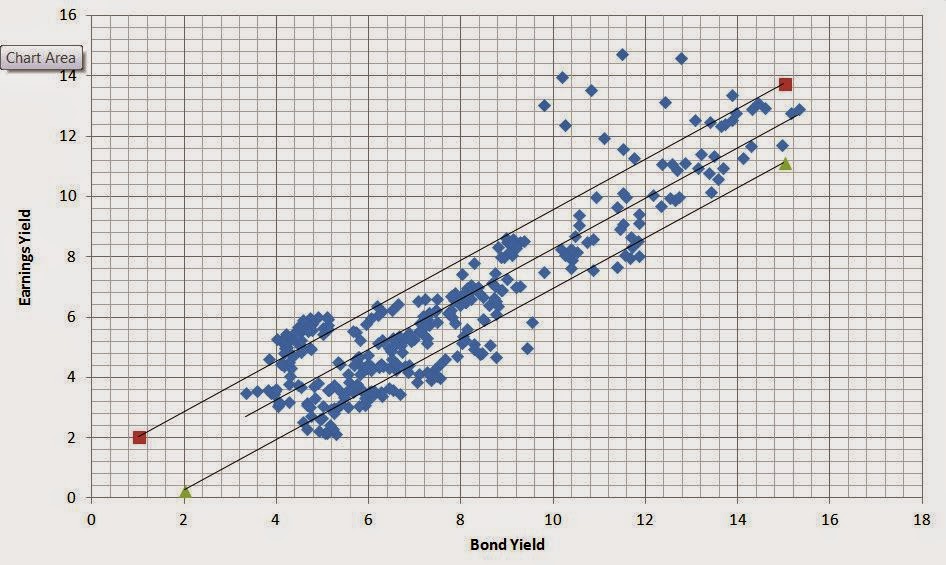

And by the way, last month I put up a chart comparing stock P/E ratios to interest rates. And then I showed the range of P/E ratios when interest rates were in certain ranges. I was too lazy to actually put bands around the regression line since it’s not a ‘one button’ option in Excel.

But I did eventually put bands around the regression line so I thought I’d put it up here. It doesn’t really change the conclusion very much, of course.

This is data from 1980 – 2014. The data seems cherry-picked for an expensive time, but including data after 2007 and before 1980 would show that interest rates are even less meaningful (lower R2 etc.). Since we are trying to figure out what higher interest rates would do to the market, it’s fine.

Those red squares don’t mean anything. they are just the end points of the upper band.

And here is the table of the respective lines (the regression was y = 0.8367x – 0.1 with an R2 of 0.77):

|

IR

|

P/E

|

-1std

|

+1std

|

-2std

|

+2std

|

| 1 | 135.7 | 48.9 | 30.0 | ||

| 2 | 63.6 | 34.7 | 379.7 | 24.0 | |

| 3 | 41.5 | 26.9 | 90.9 | 20.0 | |

| 4 | 30.8 | 21.9 | 51.6 | 17.1 | 154.6 |

| 5 | 24.5 | 18.5 | 36.1 | 15.0 | 67.4 |

| 6 | 20.3 | 16.1 | 27.7 | 13.3 | 43.1 |

| 7 | 17.4 | 14.2 | 22.5 | 12.0 | 31.7 |

| 8 | 15.2 | 12.7 | 18.9 | 10.9 | 25.0 |

| 9 | 13.5 | 11.4 | 16.3 | 10.0 | 20.7 |

| 10 | 12.1 | 10.4 | 14.4 | 9.2 | 17.6 |

| 11 | 11.0 | 9.6 | 12.8 | 8.5 | 15.4 |

| 12 | 10.1 | 8.9 | 11.6 | 8.0 | 13.6 |

| 13 | 9.3 | 8.3 | 10.6 | 7.5 | 12.2 |

| 14 | 8.6 | 7.7 | 9.7 | 7.0 | 11.1 |

| 15 | 8.0 | 7.3 | 9.0 | 6.6 | 10.2 |

The regression line shows that at an interest rate of 6%, the P/E ratio of the market is 20.3x. The 1 std range around that is 16.1x – 27.7x.

I know there are arguments that margins are too high, that absolute valuations are more important than relative etc.

But what I am trying to show is simply that there is no reason to think that markets must go down just because interest rates back up some. There will be some short term volatility, of course, as people adjust their portfolios. If interest rates go up a lot, of course, the stock market can go down a lot too.

Valuation Fallacy

I think there is sort of a fallacy when looking at long term valuation charts. People point to 1929 and 2000 and go, wow, every time the market gets over 20x P/E, there is a big bear market. And look, every time the market trades at 7x P/E ratio, a huge bull market follows. And people conclude that a market with a 20+ P/E ratio must be followed by a bear market (in short order), and the best time to buy stocks is when the market is trading at 7x P/E ratio.

Well, buying only when the P/E ratio is at 7x and not owning stocks when the market is over 20x wouldn’t have resulted, I don’t think, in good performance over the long term.

This reminds me of that bank robber and gun fallacy; just because all bank robbers have guns doesn’t mean that all gun-owners are bank robbers.

So What to Buy?

A couple of years ago, I said that Buffett would keep buying Wells Fargo up to 10x pretax earnings (see post here: Wells Fargo is Cheap!). I said he would be buying it up to $50/share back then (the stock was at $35).

Updating this figure, WFC earned $6.00/share or so in pretax earnings in 2014. So Buffett would keep buying WFC up to $60/share. Keep in mind that this is not intrinsic value, but what Buffett would gladly pay for the business (and sure enough, he bought more shares in the first quarter of 2015).

For JPM, using the same metric, Buffett would gladly pay $74/share; JPM earned $7.40/share in pretax earnings in 2014.

So this is not some valuation that is adjusted up for interest rates or anything like that. I showed that Buffett often pays 10x pretax earnings even for listed stocks (and not just private businesses), and this has occurred over decades.

These are stocks you can buy now that Buffett has proven to be comfortable with at price levels that are consistent with Buffett’s valuation levels that goes back a long time.

And these banks, I don’t think, have unnaturally high and unsustainable margins (what many feel about the stock market overall). In fact, banks seem to be underearning due to the still subdued housing market and more importantly, the unnaturally low interest rates. So there you go; an actionable idea to go along with this long opinion piece.

Conclusion

Jamie Dimon is a great CEO and is massively, ridiculously and obscenely underpaid. And you can have him work for you at a reasonable valuation too!

Appreciate your posts. Walmart trailing four quarters pre tax income is 24 billion. Current market cap is 240 billion. This is right in the Buffett buy range

CEO's pay should not be based on percentage of profits but on how much it would cost to find somebody as good or how much would somebody else pay Mr Dimon. I think the pool size of people as good as Jamie Dimon is quite large. Finally about scandals, so far people have not been after Mr Dimon for telling to his traders that he was instructed by the fed to lower his interbank lending rate. Of course, they took positions based on this piece of confidential info.

I don't know if it's a good idea to link pay directly as a percentage of profits, but it's an indication of how well paid someone is.

As for the pool size for people as good as Dimon being "quite large", that's a surprising comment. I would love to know who would fit that bill!

As for communications between a bank and it's regulator, I don't know how that works. If the Fed guided the bank to do something, you can't prosecute them for doing it. There is a lot of communication that goes on between banks and regulators (and primary dealers and the Treasury).

Thanks Brooklyn. Nice to hear from/read you. I felt sure you would have something to offer on Dimon's recent commentary. I keep wondering why Buffett (or rather BRK) doesn't own any JPM (I know he owns a few shares personally). I suppose perhaps that he's focused on the deposit bases of BAC and WFC as the "moat" or as close as it gets in this business.

Buffett has said on CNBC he bought 1M shares of JPM in his personal account. The reason he bought JPM instead of WFC is because he already bought WFC for Berkshire and he doesn't want to create a conflict. he also said he bought WFC instead of JPM for berkshire because he thinks WFC is better than JPM.

Yeah, thanks for the reply. The personal investment was what i was referencing. His explanation just sounded like a polite demure to ne. Once he converts the bac investment that will be up there in like the top five (700 million shares or so i think). Bac is more of a direct competitor to wfc it seems so the conflict thing is unpersuasuve to me.

Good question about Buffett not buying JPM for BRK. I think the main reason is because his JPM ownershjp is simply because he is a big fan of Dimon and that can be a problem if he owns a huge position in BRK and Dimon retires. If you look at WFC and GS, for example, they are proven franchises through generations of CEOs.

As for BAC, that was clearly a special situation. I don't think Moynihan is that great, actually, and Buffett doesn't mind; as long as he cleans up the legal mess, cuts costs and gets BAC on track, that's all that he needs to do. And he was able to grab a big chunk of it at way below tangible book with a sweet deal.

JPM the investment bank has a decent reputation going back, but the money-center bank side hasn't been so great, I don't think, until Dimon came on board.

So that's my guess on why BRK doesn't own JPM…

This comment has been removed by the author.

BI,

I really like your posts, which provide a fresh perspective on companies I might or might not have had on my radar.

I think that one of the downsides in increased ownership of securities by passive index funds is the idea that these managers do not do the research to know how to vote. I am afraid they follow proxy advisory firms, because indexers are taught early on that effort doesn't pay. This creates perverse incentives however, as I am also afraid large institutional holders like index funds let management just pay themselves a lot of money, without really earning their keep. Of course, in Dimon's case, you have demonstrated that he earned his keep.

So you're saying that $20m a year is to be "massively, ridiculously and obscenely underpaid."

Right… That's what happens when thinking is confined to financial figures and ratios, forgetting all about the real world out there. Dimon's comp. and his peers' comp. are all outrageous as it is. And this ugly trend just keeps on going..

And no, I don't think you should worry about Dimon leaving his job because of underpayment…

Too bad there aren't real regulators putting an end to this shame

Most people I know agree with you.

Just for fun, I googled "highest paid CEOs" and saw the AFL-CIO list of the top 100. JPM is not even in the top 100. Goldman Sachs and Wells Fargo were not even in the top 50; actually it's at the bottom of the list.

So it's not just financials. I have no problem at all with pay for performance. People were disgusted that Mayweather got $100 million for a single fight. Others hate that some movie stars get $20 million for a single movie (maybe not anymore!).

I have no problem with any of that. It's a free country and if people are worth that much, so be it.

As for corporate CEOs, I too believe that things are out of control. Believe it or not, I do tend to the progressive side on social issues.

But ISS is not in the business of social engineering; they should not be making decisions based on what they think CEOs in general should be earning.

The job of the BOD is to make sure we have the best CEO we can at fair compensation, just like a manager of the NY Yankees. I think nobody would disagree with the notion that that team is grossly overpaid. But you won't make a winning team by saying, "I think no baseball player is worth more than $400,000/year; I don't give a crap what track record they have!!". This may get an applaud from me (not being a baseball fan). But you won't get into the post-season.

Anyway, I understand your viewpoint; most of my family members and closest friends agree with you (and disagree with me!).

I don't have a view as to whether Dimon is a good or bad CEO or whether he is overpaid or underpaid. However, I do believe that the charts you posted in this article are not helpful in making either determination. Consider the following:

1) The "Sustained Earnings and TBVPS" chart: those are pretty nice CAGRs with the HUGE caveat that the starting point is 2008. Nice try.

2) The "TSR" chart: JPM beats peers. That's nice, but TSR for JPM shareholders over this period is only 7.7%. That would be lower than my required "cost of equity." Sure, on a relative basis, he beats his peers. So, let's say that relatively, Dimon should be paid more than his peers. I would argue that the peers should get "very little" and that Dimon should get more than "very little." This chart does very little to tell me whether $20MM (or whatever it is that he gets) is the right absolute amount. Oh, and for those of you that will bring up the "hey, it was a financial crisis, it wasn't his fault, and returning 7.7% through all of that is very good" — I don't disagree: relatively, he did well and should get paid more than his peers. As for the financial crisis part of it, if you want to lower the bar in bad macro years, we need to agree on raising the bar in good macro years, too. Deal?

3) The "% of Profits Paid to CEOs" chart: really?! Wow. A cashier at Walmart earning $8/hour makes less in % of profits paid to her than the cashier at the corner deli who also makes $8/hour. The profits of the company are in large part driven by the dollar value of assets they have in place. CEO/worker comp should not be calculated off of a percentage of that since CEOs/workers at bigger institutions will appear to be underpaid regardless of their skill.

4) Which brings me to my final point. The only chart that really is illuminating is the chart on the bottom right hand corner of the "Alignment" slide. How much value did Dimon and his team actually generate? To do this, you need to do the EVA analysis…ROIC – WACC (or similar analogue for banks). The bottom right hand chart at least is a good starting point for this. Everything else is just sales-y BS and we should call it that.

3)

Good points. Thanks for the counter view. I can't respond at length here in this comment box, but here are some quick answers.

1) If you look back at some of my other JPM posts, you will see that the consistent growth in BPS starts before 2008 and there is no downtick, so 2008 is not a low point in terms of TBPS; JPM never lost money throughout the crisis. So this is not the same as looking at great returning funds since 2008 (after having lost 50% during the crisis). JPM never had such a book value drawdown.

2) Well, I'm not sure what to say here. He did better than his peers. He is a better CEO in my mind than most other financial and non-financial CEO's. As a shareholder or board member, you want the best CEO as possible to run your company. You don't go, oh, you didn't meet my 10% hurdle so you don't get paid. Well, if you do that, the CEO leaves and who knows who will run the business. Having spent my career in finance, I can tell you with confidence that most of the time, you don't want to replace a highly paid employee with a cheaper one unless the employee is purely clerical or noncritical, non-front-office etc. When you run a baseball team or basketball team, you can't say, well, I don't think he's worth xxx so I will offer yyy. Well, another team will pay xxx and you probably won't have a very strong team (despite what you read in a Michael Lewis' book).

3) I agree with you in the case of Walmart because the cashier is totally fungible/replaceable and as far as I'm concerned, a totally unskilled job. But any job that requires skill is not comparable at all. Unskilled work will always only be worth the lowest wage. Skilled work, however, will not work that way. When you want surgery done on your child, you aren't going to shop by price; cheapest surgeon etc… You will want the best. Same with running a company. Dimon is arguably the best CEO that has ever lived, and in that context his pay is very modest. GE has arguably the worst CEO that has ever lived (well, OK, not worst because the worst ones are in jail. But yes, that guy to me is pretty awful) made like $40 million. There might be some one time stuff in there, but this guy has created no wealth at all and is just horrible, I think. I like him cuz he seems like such a nice guy. But as a CEO, I don't know, he seems terrible. Google top paid CEOs. In any case, if you want to build a world class company, you have to pay up. That's just the way it is at the moment. And I, as a shareholder, am more than happy to pay Dimon (and I say this as a shareholder, not as an armchair critic who has nothing on the line).

4) Dimon and his team creates a lot of value. I think EVA, WACC and all that stuff is nonsense. What you call as salesy BS to me are simple facts. I spend a lot of time reading annual reports and proxies, and very few companies actually explain why their CEO gets paid so much. It is actually quite refreshing how well JPM explains this stuff. Look at countless other companies that pay their CEOs a ton while their stock price goes down, the company loses money and have ROE lower than their peers etc… with stock prices that have done nothing for years.

It's very easy to sit there and criticize these things, but if you see what's out there, you will see that JPM is really a well run organization with very good disclosure and explanation about everything they do inlcuding CEO compensation. I wish all companies were this clear and well run.

Anyway, there is more to say, but it's hard to work with these comment boxes so I'll stop before something happnes….

Great post – as always.

Is Dimon really underpaid? Or are the other CEOs just massively overpaid? Given that it has been reported that Mr. Dimon now has a net worth over $1 billion, I would venture that he has probably never been underpaid in his career. I have a problem in general with CEO compensation (really all C suite comp) as I find that most CEOs create very little long-term value, are merely "tending the garden someone else planted", and have very little real skin in the game. The options and restricted stock schemes that are prevalent today are nothing more than a heads I win, tails you lose compensation arrangement. I have no problem with someone getting wealthy by creating something of value that makes life and society better, but let's be honest, most CEOs have created nothing.

I do think so. Read my response to similar comments above.

KK,

Have you looked at Ametek (AME)? Looks like another "outsider" kind of company. Francois Rochon, a pretty good Canadian value manager, talked about it in one of the most recent issues of Value Investor Insight. He described it as a mini DHR.

Hi, Yes, I took a look at it as someone mentioned it when I posted about the outsiders. It looks interesting for sure. I don't own it at the moment, but I should take another close look.

If a Walmart employee beat up an annoying customer, that employee would probably go to jail. Walmart would not be charged, unless it was proven that Walmart management encouraged such behavior, or maybe that management was negligent in hiring a dangerous person or something like that.

Are you saying that banking culture, fiduciary duty, and, at times, direct orders aren't causing any of these banking violations. Outside of employees disobeying orders, employees really shouldn't be arrested for doing their job. I think this point of view does not consider the consequences of the strong stance. Even if you believe the buck should stop with someone, how do you arrest someone that is playing within the rules of the system. You could also make a comparison to waving alcohol in front of a former addict and then punishing them for giving in.

If an boss orders a subordinate to do something illegal, then the employee should refuse. They can even go to the CEO or legal department or call the whistleblower hotline, go to a regulator etc. The employee that refused should not go to jail or get fired, the boss should get fired.

My whole career was on Wall Street, and for me, it has always been pretty clear what is right and wrong from a legal standpoint. There were a lot of gray areas, but when things were gray, we spent a lot of time in the legal department to get clearance. These legal issues were not anything to do with ethics, though, more just about tax and technical legal issues (U.S. entity dealing with offshore entities, tax consequences etc…).

It's a bit complicated to discuss in these small comment boxes, but the taxi company analogy is the easiest for me to describe. Yes, the culture can be competitive etc, but if one of your drivers ignores a red light and runs over and kills someone, that cab driver should get fired, go to jail etc. Did the cab company push drivers to increase fares? Probably. Did the company encourage employees to ignore traffic lights or otherwise do whatever is necessary to increase fares? If yes, then that is a company-wide problem. Otherwise, it's the driver.

Maybe I am lucky, but in my career, even though I've seen things get funky, I have never had a boss that encouraged illegal activity. To the contrary, everyone was pretty cautious. The culture can be competitive, but we had many legal and compliance meetings warning us not to cut corners etc…

I did see people do things that were not cool, but that sort of behavior, from what I saw, was not encouraged from higher up. It was the decision at the local level; some aggressive person wanting to put up big numbers willing to do whatever they can to do it etc…

On BAM, my understanding is that they have a dual share structure with management controlling things rather than a shareholder-friendly arrangement. Even though they have wonderful assets and a nice track record, their dual share structure waters down the margin of safety a bit it seems.

Reliance tops the Nifty weightage list after six years,

Equity Tips

Never give up. Today is hard, tomorrow will be worse, but the after tomorrow will be sunshine.

Equity Tips