Crazy!

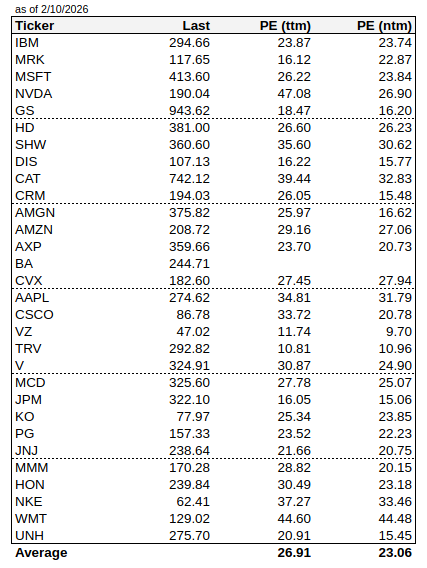

It seems the market is going crazy, as usual. So I decided to do something I haven’t done in a while; look at the Dow 30 stocks and their P/E ratios one at a time. Averages often don’t always tell the whole story, but looking at a list of individual stocks can give you an idea of what’s going on.

The DJIA P/E is 24.7x (ttm) and 21.1x (ntm), and for the S&P 500, they are 25.2x and 21.8x. With 10-year treasuries in the low 4%, it is totally normal and reasonable to me. I would bet Buffett would say the market is in a “zone of reasonableness”. The following is the list of the Dow 30 and their ttm and ntm P/E ratios. I excluded BA because it’s ntm P/E is like 6000+, and it makes the average P/E meaningless. Accuse me of manipulating data; that’s fine with me. Since I just did a simple average, the number differs from the index P/E that I grabbed out of the WSJ. To make it comparable, I would need to price-weight it, but I won’t bother.

Dow 30 P/E

Here’s an interesting thing to look at. We know that Buffett is price sensitive and will sell things when they get silly. I actually think the sale of AAPL and the current huge cash position is just a function of rebalancing the portfolio as AAPL just got way too big. I know he says he doesn’t do that sort of thing, but he does adapt to reality and will do things even if he says he wouldn’t (bought Apple after years of saying no tech!). The fact that he still left AAPL as the largest holding suggests that.

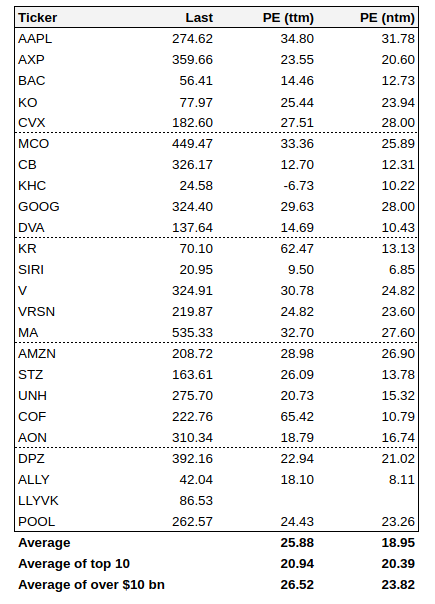

BRK Holdings P/E ($1 bn+ positions)

It is interesting because if you look at the P/Es of BRK holdings, they are not that far off from the market itself. For all positions exceeding $1 billion (based on September 2025 positions), the ttm and ntm P/E’s are 26x and 19x repectively. So, yeah, forward earnings is definitely cheaper than the market, but if you look at the top 10, forward P/E is 20.4x and for positions over $10 billion, it’s 23.8x, not so far off, if not higher than the market itself.

I know Buffett/Munger have said the hurdle is higher to want to sell stock because you have to pay taxes on it and the return on the alternative has to be good enough to make up for that. But if things are crazy and absolutely certain to go down or have very low returns over the long term, there is no doubt he would sell.

Given this, if something is good enough for Buffett to own / hold now, that is telling us something. It doesn’t mean Buffett would buy at these prices. At the very least, he is telling us that these stocks at these prices are certainly not overpriced tulips.

Looking through this list, there are some interesting ideas, like CB is cheap, isn’t it? This is not the old CB that we all used to know due to the 2016 ACE deal, but it may be worth a look. I know many of you have been following it, probably, because it’s an insurance company, and it is an often rumored BRK acquisition.

As an aside, one regret for me is MCO. MCO was a villain during the financial crisis and it was toxic. It is very interesting that Buffett never sold it. I noticed then that the damage to its reputation was mostly limited to the structured products area. Their core bond rating business didn’t slip down that slope of selling ratings for cash, or at least to the extent that it did in the structured area. All the bad ratings and loss of credibility was in MBS, CDOs, CLOs and things like that. So even then, I had a feeling that over time, they would recover based on that core business as it was obvious even back then that debt issuance around the world will just keep growing. I have not been following this closely, but I should have been, especially since the financial crisis as I did have that clear variant view. I’m not sure why I didn’t act on it. Well, it’s true that I did pile into JPM (at $20!) and things like that, so it’s not like I didn’t do anything back then.

But here’s another way to think about this. BRK owns MCO now at this valuation, and it’s not like it has supercharged growth. Is it a stretch to argue that if Buffett is fine owning things at these levels, that we can’t be looking at other companies at similar valuation levels? Is 25-30x P/E so bad? I personally am not averse to these valuations, as you know, since I have been saying 20-25x for the market is totally fine. But it’s just some food for thought.

AI Insanity

I am reading the same articles you are, about all this capex going into AI. And yes, I am getting a little nervous too. I haven’t listened to the recent tech earnings calls yet, but for some of the big guys like GOOG and AMZN, the good thing is that as they invest in data centers, they can use this for their own business too. If you are OpenAI or other AI company that is investing massive amounts for a single purpose and it doesn’t work out, that is much riskier to me than a hyper-scaler investing as they can redirect capacity to various other lines of businesses or use it internally. But, I agree, some of these numbers are getting huge. I don’t know how this is all going to end. AI evangelists will tell you it won’t end for a very, very long time, as it is just incredible what it can do.

I’ve had people show me stuff that looks like professionally written software that they created using chatGPT (Claude is better for coding). The only problem is they didn’t know how to deploy it into the real world. So I just suggested prompts for one of them, and told him what to ask chatGPT to do; like how to register a domain name, how and where to get a virtual machine to host it cheaply. How to make the domain name point to the virtual machine, how to create a user login system with a database etc.

I use chatGPT, Perplexity and Gemini now all the time too for many things. It is really handy. For example, I have a few of these cheap Citizen and Casio watches, and I can never figure out how to go back and forth from DST to EST. And I used to spend a lot of time reading the manual trying to figure it out. Now, with chatGPT, I can say, “How do I set my Casio xxx model to DST?”, it gives me a step-by-step that actually works. I used to have to go through the manual, failing that, go to Youtube and watch video after video, nope, doesn’t work etc… Now, chatGPT, and boom. Done. Doesn’t take me more than 30 seconds. Yes, I know, that’s really trivial, but you do this for various tasks during the day, and you are talking about saving hours of time.

In the coding world, we all know how bad a lot of documentation is. Sometimes, we can spend hours just reading through documentation trying to figure something out. Now, with this AI, you can get an answer in seconds. No more poorly written documentation, outdated information or spending hours scrolling through years of Stack Overflow threads (and finally finding a solution that works for you at the bottom of a very, very long thread, the 23rd one you scrolled through). It is amazing. It’s like having an assistant working for you, but when you ask them to do something, they can respond in seconds. It’s kind of scary. I use it all the time for tax and legal issues too. Of course, I cross-check the various AI and make sure they agree, and I can ask for the source so I can actually read the relevant law. I wouldn’t want to represent myself in court with my laptop and chatGPT in front of me, of course, but for most minor things that we all need to ask, it is very useful, and oftentimes it is more than enough information to get comfortable.

Developers could probably relate, but recently I was stuck on some code and it kept throwing errors and although I consider myself pretty good at debugging, I just couldn’t figure it out, and out of frustration I cut and pasted the whole code segment into chatGPT and it found the bug right away. This is not ideal; I don’t want to be posting my code into some black box, but there was no personal information or credentials anywhere so figured it was fine. Some will read this and say, hey, use a good IDE and relevant plugins/extensions and you will never have that problem! But, OK, that’s another separate long topic.

Berkshire Hathaway

I know, there is a lot to talk about with BRK. Buffett is no longer the CEO. I wonder what the annual report is going to look like. I had totally forgotten about it, but I started another post on this topic and it’s in the queue. I may finish it up and post it later. But for now, I would just say that Buffett’s stock-picking skill hasn’t really been a factor in a long time, except AAPL (huge one!), and he was pretty hands-off with the operations. So it may not be a bad thing that a more hands-on operator takes over. It is possible that some things can actually improve at BRK. While Buffett’s greatest skill was limited by the sheer size of BRK (he was only able to realistically look at 100 or so names as potential investments to move the needle, private deals limited by competition from private equity etc.), Greg Abel is not restricted in that way. He can dig into operations and make them more efficient, for example. So while Buffett’s skill was getting less and less useful as BRK got bigger, maybe Abel’s skill gets more and more useful as they get bigger. I don’t know if the second part makes sense, but it sounds good so let’s leave it in there.

But my point is, BRK may not lose as much as we think in terms of Buffett stepping back, but may have a lot to gain by Abel, perhaps doing things that Buffett would never do. Who knows, maybe it is time to centralize and standardize operations across some of the subsidiaries to gain efficiencies. Maybe it is time to sell off or close businesses that are not returning the cost of capital. The BRK reputation of not doing such things to attract great private businesses may not be so important anymore as they are just far too big to depend on finding such businesses. It’s just a thought. I don’t mean Abel should become like Chainsaw Al, or, say, do zero-based budgeting for all subsidiaries. But there is a lot of space between that and totally hands off “almost to the point of abdication”.

Anyway, it will be an interesting year. I can’t wait to see what the BRK annual report is going to read like, and what the annual meeting is going to be like. Will it still be the Woodstock of Capitalism, or will it be dramatically reduced?

We’ll see.

Always look forward to your posts. You’ve replaced OID as my randomly, but appropriately timed voice of sanity.

Buffett did actually sell some MCO after the financial crisis go back and check the records. I believe he did it to demonstrate to Management that their behavior was not appropriate although I don’t think he sold a lot maybe 15 to 25% of his holdings something like that.

Thanks for the correction. He does buy and sell around his positions sometimes. But the gist of it is that he held onto most of his position. He did dump all of GS, even after saying at an annual meeting that he feels it in every bone in his body that GS will come back and make a lot of money. Maybe he should have sold BAC and held onto GS instead…

I believe his post financial crisis MCO sales were primarily around getting it below equity method levels and to remove any appearance that MCO was somehow not going to be unbiased in rating BRK’s debt issues if it was looking more and more like a subsidiary. I believe BRK was over 20% at one point – 15% from the D&B spinoff and then years of MCO repurchases.

Thank you for sharing your insights, always a good read.

Thanks for this – always a good read. Just wanted to add that Buffetts’ adventures in Japan have showed he can still find amazing things, but agree that if Abel can do some gentle restructuring, it could be a good thing. However, I still fundamentally worry as, time and time again, we’ve seen that succession is hard (It would be interesting to see a list where it’s actually worked).

Yes, that’s right. I’m getting sloppy. The Japan trade was a good one! But the overall point is, it’s not like the equity portfolio is beating the market by 1000 bps per year like in the old days, and that is going to go away all of a sudden. The outperformance premium of the stock portfolio has been going down for years, if not underperforming in recent years. Even with some of these great bets now and then, it is not going to get stock return outperformance back to where it was in the past…

Still, the APPL and Japan trades have added significant value to BRK so can’t knock it.

Thanks, great read. As always.

Just some random thoughts to some of the points you make:

1. Yes, AI makes things just more easy and it feels like saving time. That’s obviously what all of us are experiencing. But the question is: where will the free time go? Will coders simply have to do more tasks in the same amount of time? Will they write better code? Will there be more digital assistants? It should definitely lead to a jump in productivity. But how will our private lives change overall, and will it make us happier? I mean, there are so many inventions that have saved us time: washing machines, dishwashers, vacuum cleaners (robot vacuum cleaners), hot water from the tap, the telephone, fax instead of letters, email instead of fax/letters, teams, digital calls. Working from home saves travel time to work. But do we all have more time? Or do we just spend even more time on the screen? That wouldn’t necessarily be good for our mental health, but I find it difficult just to maintain the screen time I had before AI, not to speak of less. Are we perhaps simply finding better solutions at work and in our private lives and – since the hurdles are so low – investing even more time? So far, the latter has been my observation. I can now make much more informed decisions or easily question expert advice (insurance, photovoltaic system for the house) with just 20 minutes more effort here and 5 minutes more AI help there. I go into a depth that I would have spared myself in the past, instead of reading a book or doing more sport again. But maybe that’s just me (I hope so).

2. CB. Yes, very cheap if compared to others. Some Insurance companies even more. Fairfax currently delivers ROEs of around 20%, and in the long term certainly north of 15%, but with a PB ratio of 1.25 you get to a PE ratio of 6 (ROE 20) to 8.3 (ROE 15) if I use your previous posted calculation method probably a decade ago… A PE ratio of, say, 7 for a company with an ROE of, say, 18. AND with returns of 47% (2021), 32% (2022), 55% (2023), 66% (2024) and 23% (2025) in the rear-view mirror. Crazy! I get a sense of how Shelby Davis must have felt in the 1940s, even though I was nowhere near as focused as he was unfortunately. Anyway: What would be a reasonable valuation for a company with a ROE of 18% and a P/E of 7?

– A doubling of the share price would mean a P/E ratio of 14 (rather a joke for a company with ROE 18),

– A tripling tomorrow would be cheap, four times okay,

– Even quintupling today’s price tomorrow, I’d find reasonable if the ROE were to be sustainable in the long term. Let’s just do the math: After five folding tomorrow there would be a company with a pe ratio of 35 and ROE18. But in 12 years, profits would increase eightfold (rule of 72 tells us at 18% it’s doubling every 4 years); if the share price only doubled in those 12 years (so a ten bagger from todays price within 12 years and 6%/year over a decade), that would again be todays P/E of 7 (PE Ratio of 7 today x 5 times is a PE Ratio of 35. => 8 times earnings of today would be a pe ratio of 3.5, so a double in share). 6% annually – that’s not what we like to invest in, right? So Quintupling tomorrow we would have to sell, don’t we? BUT.. no…: Why should a business with ROE 18 in the rearview mirror being priced at P/E 7 in 12 years? Well, I don’t know, but that’s the valuation where we are today and we have ROEs above 18% on average for the last couple of years in the rearview mirror. It could of course be valued at least with a pe ratio of 14 in 12 years than (so a 20 bagger from today and a return of 12% annually AFTER quintupling tomorrow) P/E could even be higher, see above, so that gets us to a 30 or 40 bagger in 12 years, if we just get to P/E of 21 or 28? But that can’t be true…?! But if it would be like that and the multiple would stay so low for the whole time, they could even accelerate ROE well above 18, just by buying back stock, which is actually what the are doing. Which would bring the P/E even more down 12 years down the road, so the multiple should be even higher, but … (Everybody has to do his own due diligence) Well, that’s a crazy circle in which I quickly think. But is it realistic? Is it unrealistic? What does the market know, that I don’t? Or is my math wrong? Or is this just Mr. Market going crazy again?

Good question about Fairfax. I still own it and it has been an amazing run. I guess the market doesn’t trust he is as conservative, as, say, Buffett. Insurance is an interesting business where you don’t really know until much later what your earnings are due to reserving; I would assume that is where the skepticism is, but I haven’t been following all that closely. Watsa is known to make some wild moves, like going market neutral right before the market took off, big inflation bets (but with little cost). These things contribute to an image of a wild man, rightly or wrongly. I can easily imagine people having 80% of their net worth in BRK, but I would be nervous if someone told me they had that much exposure in Fairfax. I don’t know if that’s fair, but that’s just my gut reaction. But he does have a good track record for sure.

Can’t Berkshire monetize their holdings without selling them by issues Berkshire shares?

I don’t know what you mean, exactly, but separating their stock holdings would be difficult as most of that is held by the various insurance companies. As for spinning off some businesses, that is possible but something Buffett didn’t like. The friction-less, free flow of capital between subsidiaries is one of the key advantages of the structure.

It would be interesting to think about what John Malone would do if he was suddenly placed at the top of BRK. He is a master at realizing value in tax efficient ways… He has a very different style than Buffett, but who knows, maybe BRK can borrow some ideas at some point.

I mean, rather than sell KO, issue BRK shares of equal value.

Thanks for the post. Where I push back on the P/E point is with free cash flow. The Mag 7 names make up a significant portion of the overall S&P (not Dow). They are spending significant CAPEX with a depreciation lag. As a result, as with any name, it comes down to what eventual ROI is on that CAPEX spend. Could be good, could be bad. As of right now, FCF is zero for a lot of these companies. FCF yield is non existent or minimal, even with the P/E that looks fine. Not to mention all the suppliers into the data center that are potentially over earning today on potential peak CAPEX numbers. A lot banking on that investment panning out. Time will tell!

That is a fair point. Even if we look at it on an owner earnings basis, we still have to hope for decent return on the hundreds of billions invested. Only time will tell…

I always enjoy your posts.

One thing, I think that BRK loses with Buffett stepping down are the occasional reputation deals that get made when a company may be in trouble and they offer BRK a sweetheart deal just to get the Buffett stamp of approval. I’m not sure how much this moves the needle but those opportunities are probably not going to be the same

True. One thing, which is true in most ‘founder retires’ cases is big, bold moves done quickly becomes less likely. Buffett can get away with it due to his long track record. Also, nobody questions his ability to assess a situation quickly (without due diligence reviews). Nobody taking over will have that skill, and nobody will ever be handed such freedom, as if things don’t work out, it can damage the new CEO’s credibility. Buffett has such a long track record that a few bad deals was never going to affect his ability to do them. But in any case, even this, as BRK gets bigger, becomes less and less of an issue as those won’t, or can’t be all that huge in terms of moving the needle there…

Berkshire’s equity portfolio – who actually manages it?

Will it be Ted, Greg Abel, or both? Buffett has said it ultimately falls under Abel’s remit, and has made comments along the lines of “he understands businesses, therefore he understands the equity portfolio.” But realistically, who in history has ever managed a portfolio of this size and concentration on their own — even as their sole responsibility? Nobody.

To then assume this responsibility can be taken on by someone who has never managed a public equity portfolio before, while also overseeing hundreds of operating businesses and countless other obligations, seems pretty optimistic at best, delusional at worst. And similarly, expecting Todd to step up from managing ~$15bn to something orders of magnitude larger…

The $300+++ billion cash balance, ex what is needed within the insurance businesses (and growing by the day)

This is the other elephant in the room. How, exactly, is this going to be deployed — and when? Let’s be honest: nobody has a convincing answer. At some point, the opportunity cost becomes irreversible. Not many people realise that cash has approximated float for the last quarter century, meaning insurance leverage has not actually been used (which makes performance even more impressive). A traditional insurer would match liabilities and duration with bonds, but Berkshire effectively chooses an even worse allocation by holding excess cash. So what is the purpose of this extreme overcapitalisation? It clearly isn’t to fund equity purchases.

This is becoming a serious issue, and one that is not being discussed enough. A material decline in interest rates would simultaneously reduce returns on the cash pile while increasing the valuation of potential acquisition targets — the worst of both worlds. Buffett may get a pass on this, but who is going to be the one to “shoot the elephant” and deploy $300 billion meaningfully?

You are right about Abel not having experience running an equity portfolio. But I think they think about this not really as an ‘equity portfolio’ in the traditional sense, but as owning a piece of businesses. This approach allows them not to have to manage this in a traditional manner, which would require a lot more bodies. That’s what I think they are thinking.

As for the cash, it’s true that I don’t think anyone but Buffett would be able to pull the trigger on an ‘elephant’, so my guess is that over time, they would use the cash for stock repurchases… Think Loews. That’s my guess. That’s what I would do too… Simplify, centralize a little bit, modernize etc…

Thank you for sharing this!

2 comments:

– re BRK: Buffett former employee Tracy Britt was recently on Shane’s podcast.

What she shared about her experience turning around the BRK Pampered chef subsidiary was quite interesting!

https://fs.blog/knowledge-project-podcast/tracy-britt-cool/

– re private AI:

You mention concerns when pasting code into chatGPT and using AI for tax/legal stuff.

Highly recommend to try VeniceAI, it anonymises your request and routes them to the best model in a confidential way

Keep up the great work!

Thanks. Sorry for the delay in approving; to prevent spam, posts don’t show up if there is a link in it, and I just saw this today…